Ohio's Tax Code is in Need of Principled Reform

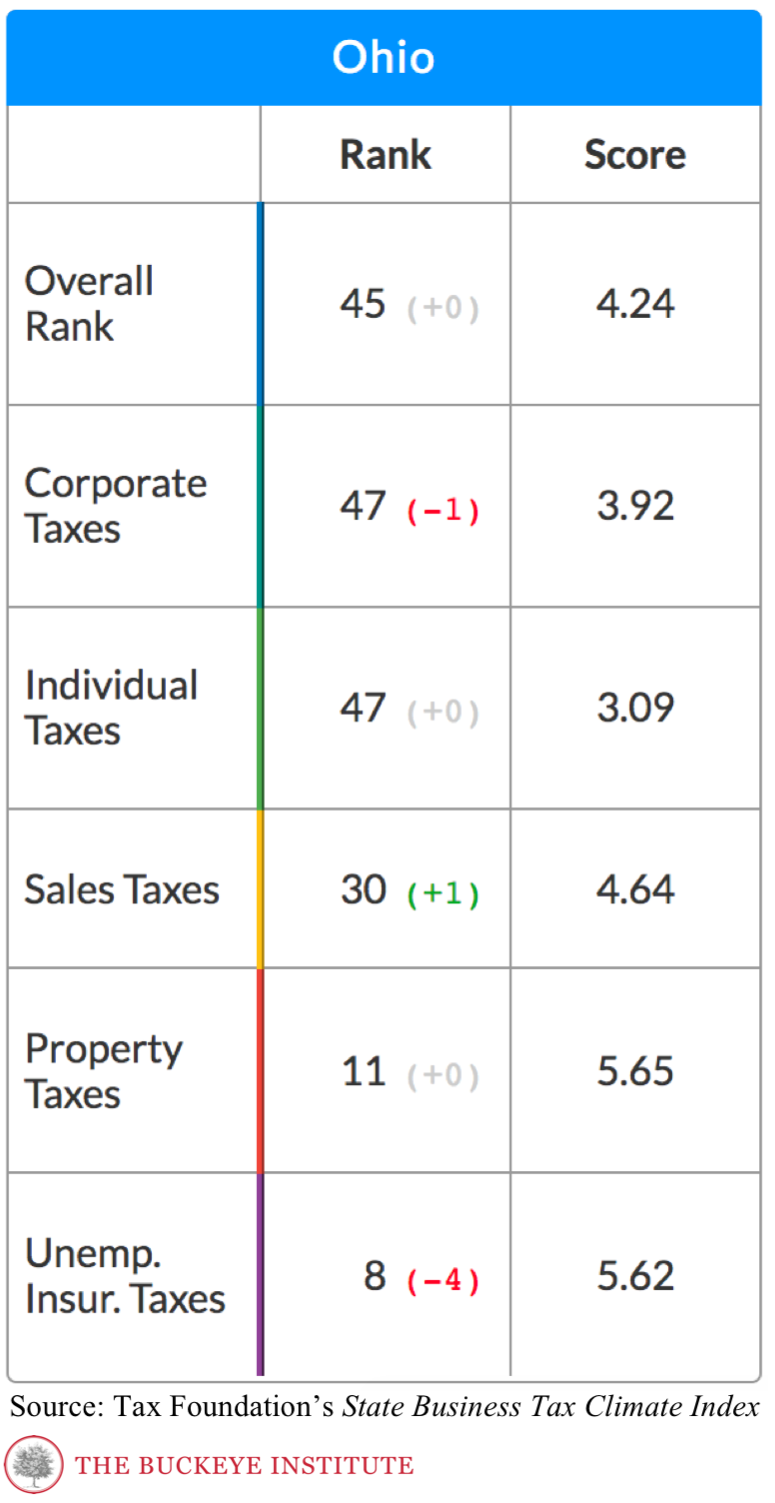

Nov 02, 2017For the third year in a row Ohio has ranked 45 in the Tax Foundation’s State Business Tax Climate Index, which ranks all 50 states based on how well they structure their tax system. According to the index, Ohio’s municipal income tax and its commercial activities tax (CAT) have contributed to creating a burdensome tax environment and have continued to weight down Ohio’s rankings.

But could it be as simple as reforming our municipal income tax and eliminating the CAT to improve our ranking? Let’s take a closer look at the Tax Foundation’s index and unpack the data. The Tax Foundation looks at five components – corporate taxes, individual taxes, sales taxes, property taxes, and unemployment insurance taxes – and scores states in each area using a 10-point scale (10 being the best).

Here is where Ohio fell in each area:

Ohio’s overall ranking is largely due to its corporate and individual income tax policies. Ohio gets hit hard for having a CAT which imposes hidden taxes for consumers. While a sales tax applies only to final consumption, a gross receipts tax, or CAT, applies to every stage of the production process, causing tax pyramiding. Basically, it is a tax assessed on a tax.

We also get hit hard in the rankings due to our municipal income tax structure, which in an op-ed in The Columbus Dispatch, Buckeye’s Greg R. Lawson called it, “the absolute worst municipal income tax in the entire nation.” Lawson went on to say, “Only 17 states levy local income taxes and of those, Ohio has the second-highest effective rate, which is layered onto the state income tax.”

The good news is, Ohio can reform its tax system to address these issues and to spur economic development and job growth. And it can do so by following The Buckeye Institute’s principles of sound tax policy, which says tax systems should be pro-growth, simple, transparent, fair and equitable. So how do we put these principles into practice? Here are some areas that Ohio policymakers should consider.

Pro-growth: As our principles state “A good tax plan will reduce tax rates on investment and labor, which are key components for economic prosperity and job creation.” And this is backed up by research by the Organization for Economic Community Development, which found that the worst two taxes for economic growth are a corporate tax and personal income tax.

This finding is backed-up by our analysis of changes to Ohio’s tax policy since 2013, which found that lowering taxes has helped:

- Make Ohio families wealthier;

- Created nearly 7,000 more jobs;

- Raised personal income by $500 million; and

- Saw Ohio’s employment rates and economy outperform most of its regional competitors.

Simplicity: Complying with the tax code should not be burdensome for Ohioans and simplifying the tax code is crucial for Ohio to experience a boost in economic growth and the removal of wasteful practices. Furthermore, every loophole, tax credit, and deduction creates an unfair special interest tax break that must be paid for by fewer taxpayers.

It is for this reason that Buckeye had longed called for the creation of a Tax Expenditure Review Committee and why its work is so critical. As our Greg Lawson said, “It is now time for Ohio’s General Assembly to get serious about shutting down tax loopholes and it is critical that they create a tax climate that is positive for job creation and helps hard-working Ohioans.”

Transparency: As we outlined in our principles “Transparency in taxation means that taxpayers should be able to easily gather information about

- Which taxes they pay (directly and indirectly);

- Why those taxes are in place, who put them into law;

- How much revenue those taxes collect and from whom; and

- How those tax dollars are used.

“Transparency strengthens the ability of taxpayers to hold policymakers accountable for their decisions and affect change when those decisions are harmful.”

Fairness and Equitability: The idea behind this is to have a tax code that treats Ohioans and Ohio businesses fairly and equitability. The tax code should not benefit or punish one group of taxpayers over another, or businesses over individuals. Corporate give a ways, loopholes, and deductions create a discriminatory tax environment and a rigged tax system. These policies also mean that when a deduction is given to one group, another group has to make-up for that lost revenue by paying more.

Ohio’s tax code currently violates nearly every major principle of good tax policy. However, through the work on the 2020 Tax Commission and the Ohio Tax Expenditure Review Committee, in addition to the work of the General Assembly Ohio has an opportunity to create a tax environment that allows Ohioans to keep more of their own money while getting the state’s economy back on track.

James Kennedy is an intern in The Buckeye Institute’s fall internship program.