New Buckeye Institute Research Outlines Policy Changes that Could Grow Iowa’s Economy by $610 Million

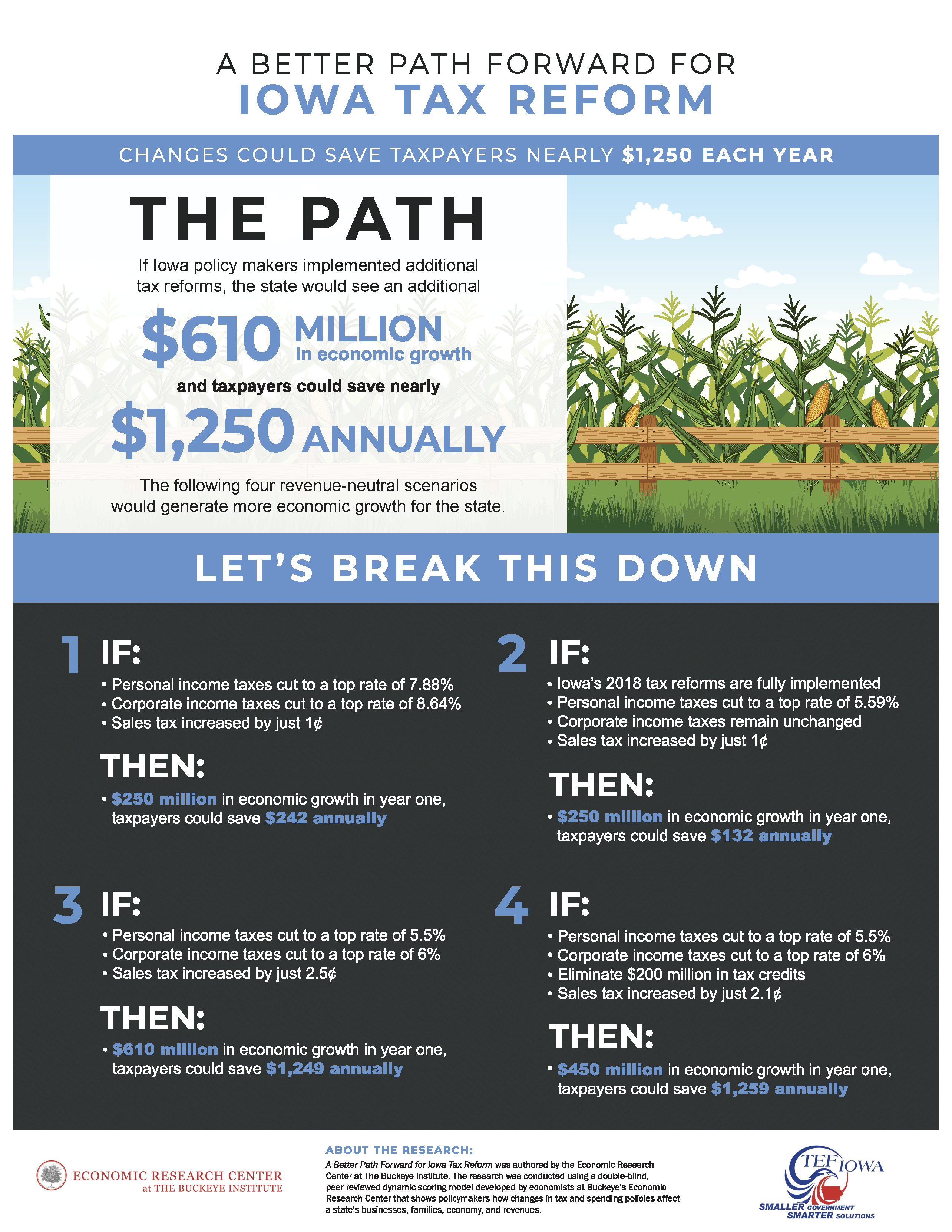

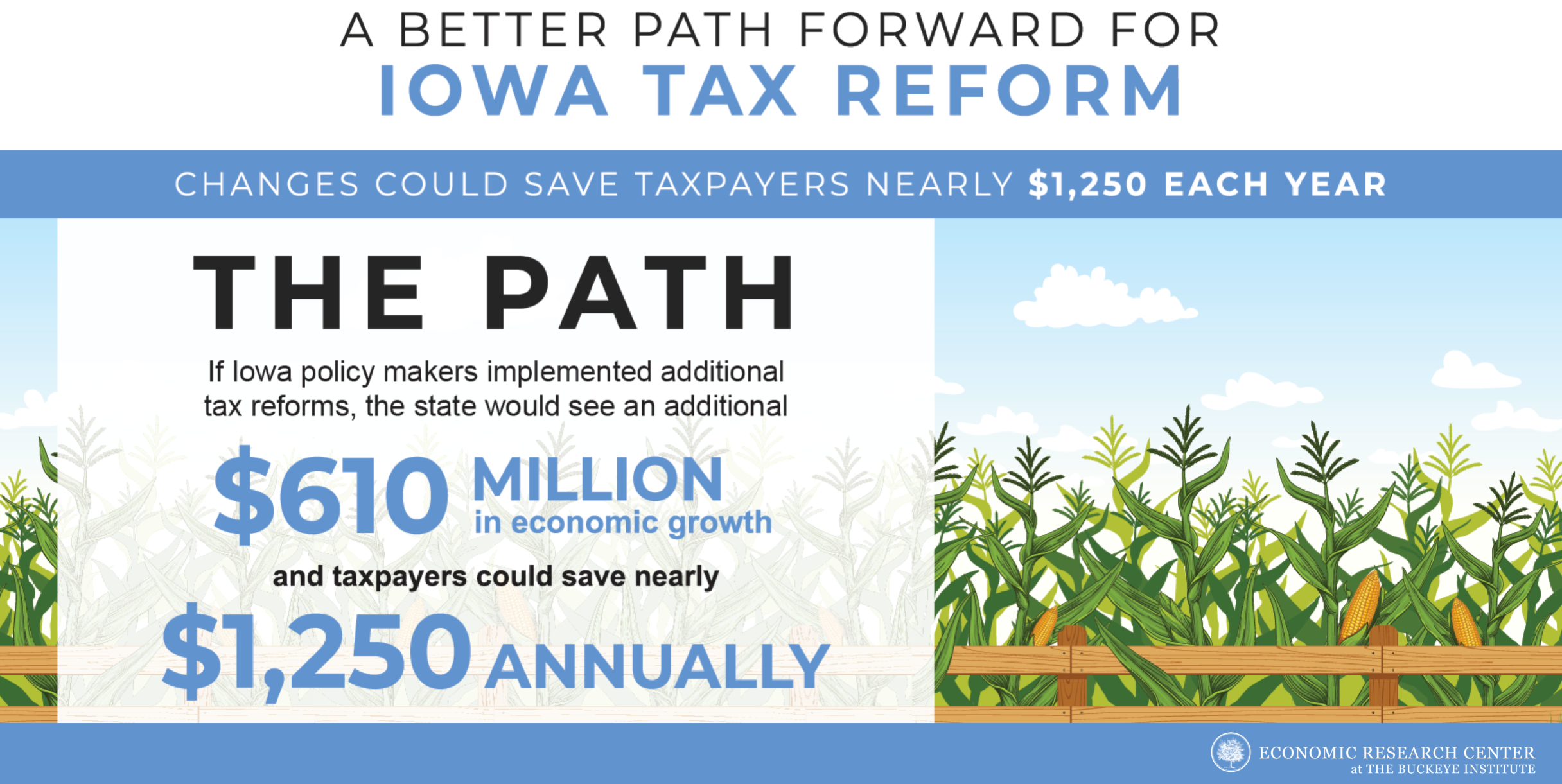

Dec 19, 2019Columbus, OH – A new report, A Better Path Forward for Iowa Tax Reform, released Monday by The Buckeye Institute’s Economic Research Center, found that if Iowa policymakers implemented additional tax reforms the state could experience an additional $610 million in economic growth and taxpayers could save nearly $1,250 annually.

The research was conducted in partnership with Tax Education Foundation Iowa, which conducts pro-taxpayer education and research and informs Iowans about the impacts of taxes and spending, and the principles of limited government.

FACT SHEET: A Better Path Forward for Iowa Tax Reform

“Iowa policymakers took a step forward in 2018 when they passed a tax reform package. But this newest economic analysis reveals that if policymakers implement further pro-growth reforms, Iowans could experience up to $610 million in economic growth and $1,249 in taxpayer savings annually,” said Andrew J. Kidd, Ph.D., economist at the Economic Research Center at The Buckeye Institute and co-author of A Better Path Forward for Iowa Tax Reform.

Using a dynamic scoring model developed by economists at Buckeye’s Economic Research Center, the report’s authors analyzed four revenue-neutral scenarios that would build on Iowa’s 2018 tax reforms, would cut more economically harmful income taxes, and would increase less economically harmful sales taxes. All four revenue-neutral scenarios would generate more economic growth for the state. The scenarios were chosen to generate further debate on how to grow Iowa’s economy and the findings give Iowa policymakers a better understanding of how each proposal would affect the state’s businesses, families, economy, and revenues. The model revealed the following effects of the four scenarios:

- Scenario One: Generates $250 million in economic activity in the first year and, on average, saves taxpayers more than $242 annually by cutting the more economically harmful personal income taxes to a top rate of 7.88 percent and corporate income taxes to a top rate of 8.64 percent, and increasing the less economically harmful state sales tax by just one cent.

- Scenario Two: Generates $250 million in economic activity in the first year and, on average, saves taxpayers more than $132 annually by assuming Iowa’s 2018 tax reforms are fully implemented, cutting personal income taxes to a top rate of 5.59 percent, keeping corporate incomes taxes at the same rate, and increasing the state sales tax by just one cent.

- Scenario Three: Generates $610 million in economic activity in the first year and, on average, saves taxpayers more than $1,249 annually by cutting personal income taxes to a top rate of 5.5 percent and corporate incomes taxes to a top rate of six percent, and increasing the state sales taxes by 2.5 cents.

- Scenario Four: Generates $450 million in economic activity in the first year and, on average, saves taxpayers more than $1,259 annually by cutting personal income taxes to a top rate of 5.5 percent, cutting corporate incomes taxes to a top rate of six percent, eliminating distortionary tax credits, and increasing the state sales tax by only 2.1 cents.

“Now more than ever states are in direct competition with one another with states across the nation lowering tax rates. Unfortunately, Iowa has high tax rates, which deter economic growth and create an undue burden for working families and businesses. In order to be more competitive as a state our rates must be lower, and this study demonstrates that building upon existing tax relief is possible and needed,” said Walt Rogers, deputy director of Tax Education Foundation Iowa.

A Better Path Forward for Iowa Tax Reform was authored by Andrew J. Kidd, Ph.D.; Rea S. Hederman Jr., executive director of the Economic Research Center and vice president of policy at The Buckeye Institute; and James B. Woodward, Ph.D., economic research analyst at the Economic Research Center.

Consistent with academic standards and methodologies, the Economic Research Center’s model has undergone a double-blind peer review and the model’s full technical description provided in the report’s appendices allows researchers to validate the model’s accuracy and the conclusions drawn.

# # #